Choosing the Right Extended Warranty To Protect Your Investment

Imagine cruising down the highway, only to hear a dreaded new rattle from under the hood. Or perhaps your state-of-the-art infotainment system suddenly goes dark. Car repairs can be costly and come out of nowhere, often wiping out your savings or forcing difficult decisions. This is precisely why choosing the right extended warranty has become a critical consideration for many vehicle owners, offering a financial safety net against the unpredictable nature of car ownership.

It's more than just buying insurance; it's about smart planning to protect a significant investment. But with countless options, confusing jargon, and varying levels of coverage, navigating the extended warranty landscape can feel like a maze. Fear not. As a seasoned journalist who's delved deep into the automotive world, I'm here to equip you with the insights you need to make an informed, confident decision.

At a Glance: Key Takeaways for Your Warranty Search

- Costs Vary Widely: Expect to pay $1,500 to $4,000, or 5-7% of your car's value, with comprehensive plans potentially reaching 10%.

- Match Coverage to Needs: Decide if you need bumper-to-bumper protection or if a powertrain plan is sufficient for your budget and vehicle.

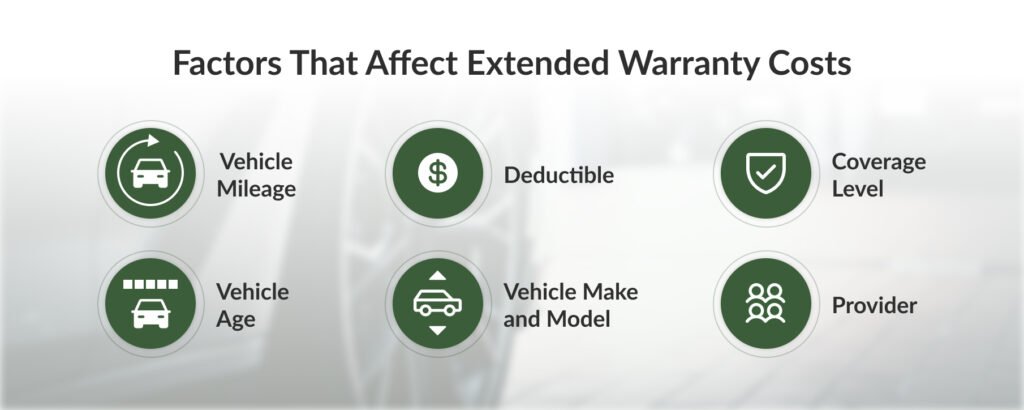

- Age & Mileage Matter: Your car's specifics heavily influence eligibility and price.

- Vett the Provider: Research customer reviews, industry standing, and claims processes before committing.

- Know Your Exclusions: Understand what isn't covered to avoid nasty surprises down the road.

- Look for Perks: Roadside assistance and rental car reimbursement can add significant value.

Understanding the Landscape: What is an Extended Warranty, Anyway?

Before we dive into selection, let's clarify what an extended warranty (also known as a vehicle service contract) actually is. Unlike your car's original manufacturer's warranty, which comes standard with a new vehicle for a set period, an extended warranty is an optional service contract that covers repairs for specified parts and systems after the factory warranty expires. It's designed to absorb the financial shock of unexpected mechanical or electrical failures, transforming potentially thousands of dollars in repair bills into a more manageable deductible or monthly payment.

For many, the peace of mind alone is worth the investment. To dig deeper into whether these plans are truly beneficial for your situation, you might want to check out our comprehensive Extended car warranty guide.

Step 1: Assess Your Vehicle & Driving Habits (The Foundation)

Your journey to the right extended warranty begins with an honest appraisal of your current situation. This isn't just about your car, but also how you use it.

Your Car's Age and Mileage: The Eligibility Gatekeepers

These two factors are arguably the most significant determinants of both your eligibility for an extended warranty and its ultimate cost.

- Newer, Lower-Mileage Cars: Vehicles still under their original manufacturer's warranty often qualify for better rates and more comprehensive plans. The logic is simple: they're less likely to break down.

- Older, Higher-Mileage Cars: As your vehicle ages and racks up miles, it becomes a higher risk for providers. This means fewer coverage options, higher premiums, and stricter eligibility requirements. Some providers may not offer coverage at all past a certain mileage threshold (e.g., 100,000 or 150,000 miles).

Be prepared to provide accurate figures, as discrepancies can invalidate your contract or complicate claims.

Your Driving Habits: How You Roll Matters

Consider how you use your vehicle:

- Daily Commuter: If you put a lot of miles on your car every day, you'll reach mileage limits faster. A warranty with higher mileage caps might be crucial.

- Weekend Warrior/Low Mileage: If your car is primarily for short trips or occasional use, you might prioritize a longer term duration over a high mileage cap.

- Driving Conditions: Do you frequently drive in extreme weather, stop-and-go traffic, or on rough roads? These conditions can accelerate wear and tear, making comprehensive coverage more appealing.

Step 2: Decoding Coverage Options (What's Really Protected?)

Extended warranties aren't one-size-fits-all. They come in various tiers, each offering different levels of protection. Understanding these options is key to ensuring you're paying for what you need, and nothing you don't.

The Big Two: Comprehensive vs. Powertrain

- Bumper-to-Bumper Warranty (Exclusionary):

- What it is: This is the closest you'll get to your new car's original factory warranty. It covers most components between your car's front and rear bumpers, with a specific list of exclusions (items not covered). Because it lists what's not covered, rather than what is, it's considered the most comprehensive option.

- Ideal for: Drivers seeking maximum peace of mind, those with complex modern vehicles laden with electronics, or owners who want to avoid high repair costs for a wide range of components.

- Cost: As you might expect, this is generally the most expensive option, sometimes costing up to 10% of your car's value.

- Powertrain Warranty (Named Component):

- What it is: This plan focuses on the most vital and expensive components of your vehicle: the engine, transmission, and drivetrain. These are the systems that make your car move, and their repairs can easily run into thousands of dollars.

- Ideal for: Drivers on a tighter budget, those with older vehicles where comprehensive coverage might be cost-prohibitive, or anyone primarily concerned with protecting against catastrophic mechanical failures.

- Cost: Typically much cheaper than bumper-to-bumper coverage, often sufficient for most drivers.

Specialized and Supplementary Coverage

Beyond the main categories, some providers offer plans that target specific areas of concern:

- Corrosion/Rust Warranty: Primarily protects against rust damage to the vehicle’s body, often stemming from manufacturing defects rather than external exposure.

- Emissions Warranty: Covers parts related to your vehicle’s emission control system, such as the catalytic converter, oxygen sensors, and exhaust manifold. These are crucial for passing inspections and protecting the environment.

- Component-Specific Warranty: Tailored coverage for particular systems like electronics (infotainment, navigation), air conditioning, braking systems, or the high-voltage battery in hybrid/electric vehicles. These can be useful if you know a specific component in your vehicle is prone to issues or is particularly expensive to replace.

When evaluating coverage, think about your car's known vulnerabilities. Does your model year have a reputation for transmission issues? Are its electronics notoriously glitchy? This research can help you prioritize the right type of coverage.

Step 3: Unpacking the Price Tag (Is It Worth the Cost?)

The cost of an extended warranty isn't just about the sticker price; it's about value. You want robust coverage for a fair price.

What to Expect for Your Investment

- Average Cost: The typical extended car warranty costs between $1,500 and $4,000. This often translates to about 5% to 7% of your car’s overall value.

- Comprehensive Premiums: For bumper-to-bumper or highly comprehensive plans, the cost can climb higher, sometimes reaching up to 10% of the car's value. This reflects the broader protection offered.

- "Good Deal" Defined: A truly good deal isn't just a low price; it's a low-priced warranty that also offers robust coverage without excluding common, expensive problems. Be wary of rock-bottom prices that hide significant gaps in protection.

Beyond the Upfront Price: Deductibles and Payment Plans

- Deductibles: Most extended warranties come with a deductible, which is the amount you pay out-of-pocket per repair visit before the warranty kicks in. Deductibles can be per-visit (you pay once per visit, regardless of how many covered items are repaired) or per-repair (you pay for each individual covered repair). Common deductibles range from $0 to $250. A higher deductible usually means a lower upfront premium, and vice-versa.

- Payment Plans: Many providers offer flexible payment options, allowing you to pay monthly rather than a lump sum. While this can make the warranty more accessible, be aware that some plans might charge interest or administrative fees for this convenience.

Always compare the total cost over the contract's life, including any fees, before signing.

Step 4: Scrutinizing the Fine Print (Exclusions You Can't Ignore)

This is perhaps the most critical section. What an extended warranty doesn't cover is often as important as what it does. Overlooking exclusions is a common pitfall that leads to denied claims and frustrated customers.

Common exclusions you absolutely must be aware of:

- Wear-and-Tear Items: These are parts that naturally degrade with use and are expected to be replaced periodically. Examples include brake pads, tires, wiper blades, spark plugs, filters, bulbs, and sometimes even clutches or shock absorbers. These are considered routine maintenance, not unexpected failures.

- Routine Maintenance: The warranty won't cover oil changes, fluid top-offs, tire rotations, or other scheduled services. In fact, most warranty providers require you to keep meticulous records of all scheduled maintenance to prove your car has been properly cared for. Failing to do so can lead to a denied claim for a covered part, as improper maintenance can be cited as the cause of failure.

- Damage from Accidents or Neglect: If your car's issue stems from a collision, improper maintenance (as mentioned above), misuse, abuse, or racing, it won't be covered. These incidents are typically addressed by your auto insurance policy.

- Aftermarket Modifications: If you've installed non-factory-approved parts or systems (e.g., performance chips, custom exhaust, aftermarket infotainment), any damage related to or caused by these modifications will likely be excluded. Some providers offer specific coverage for certain aftermarket items, but you'd need to purchase that separately.

- Environmental Damage: Damage caused by rust, corrosion (unless it's a specific corrosion warranty for manufacturing defects), floods, fires, hailstorms, or other natural events is generally not covered. Your comprehensive car insurance usually handles these perils.

- Cosmetic Issues: Dings, dents, scratches, paint chips, upholstery tears, or trim repairs are considered cosmetic and are not covered by mechanical extended warranties.

- Non-Covered Components: Even comprehensive plans have limits. Certain high-tech or luxury features, specific electronics, or infotainment systems might be excluded unless explicitly specified in your plan. Always double-check the components you care most about.

Your Action Item: Always, always, always read the sample contract before you buy. Ask the provider to clarify any exclusion you don't understand.

Step 5: Vetting the Provider (Who's Got Your Back When it Matters?)

Even the most robust coverage on paper is useless if the company behind it is unreliable. The reputation and financial stability of your warranty provider are paramount.

Here's how to research them thoroughly:

- Customer Reviews and Ratings:

- Look beyond the stars: Read actual customer testimonials on reputable sites like the Better Business Bureau (BBB), Trustpilot, Consumer Affairs, and Google Reviews. Pay attention to consistent complaints about denied claims, slow payouts, or poor customer service.

- Focus on the claims process: Are customers reporting smooth claim experiences or frustrating bureaucratic hurdles?

- Industry Certifications and Partnerships:

- ASE-Certified Technicians: Many reputable plans partner with or allow you to use repair shops employing Automotive Service Excellence (ASE)-certified technicians. This indicates a commitment to quality repair work.

- Repair Shop Network: Does the provider have a wide network of approved repair facilities, or are you limited to specific shops? The ability to choose your own trusted mechanic (as long as they're certified) is a huge plus.

- Financial Backing: Some warranties are backed by larger insurance companies, which can add a layer of financial security.

- Claim Process Transparency:

- Clarity on process: A good provider will clearly outline their claims process: who initiates the claim (you or the repair shop), what documentation is needed, and typical turnaround times.

- Direct-pay vs. Reimbursement: Does the provider pay the repair shop directly, or do you have to pay upfront and wait for reimbursement? Direct payment is usually preferred.

- Legal and Regulatory Standing:

- Avoid Red Flags: Steer clear of companies with a history of frequent lawsuits, unresolved complaints with regulatory bodies, or a sudden change in company name (which can be a tactic to shed a bad reputation).

- State Regulations: Be aware that extended warranties are regulated differently by state. Check your state's department of insurance or consumer affairs for any specific regulations or consumer protections that apply.

A provider's longevity in the market, clear communication, and positive track record are strong indicators of reliability.

Step 6: Weighing the "Extras" (Beyond Just Repairs)

Many extended warranty plans offer valuable ancillary benefits that can significantly enhance the overall value proposition, extending beyond just the cost of repairs. Don't overlook these perks:

- 24/7 Roadside Assistance: This can include jump-starts, flat tire changes, fuel delivery, and lockout services. It's incredibly helpful when you're stranded.

- Towing Services: If your car breaks down and needs to be taken to a repair shop, many plans will cover the towing costs up to a certain distance or amount.

- Rental Car Reimbursement: When your vehicle is in the shop for a covered repair, the plan might cover the cost of a rental car for a specified number of days, ensuring you're not left without transportation.

- Trip Interruption Coverage: If you break down far from home, this benefit can help cover meals and lodging expenses incurred while you wait for repairs.

- Access to ASE-Certified Repair Shops: As mentioned, many providers partner with or require the use of shops with ASE-certified technicians, ensuring quality work.

These "extras" can save you significant out-of-pocket expenses and stress when a breakdown occurs, turning an inconvenience into a manageable situation. Factor their value into your overall decision, especially if you travel frequently or rely heavily on your car.

Making Your Decision: A Quick Checklist

Before you commit to an extended warranty, run through this mental checklist:

- Vehicle Needs: Does the coverage align with your car's age, mileage, and known reliability?

- Budget: Can you comfortably afford the premium and any deductible? Is it a good value relative to your car's overall value?

- Coverage vs. Cost: Are you getting the right level of protection (bumper-to-bumper, powertrain, etc.) for the price?

- Exclusions Understood: Have you meticulously reviewed what isn't covered?

- Provider Vetted: Are you confident in the provider's reputation, claim process, and financial stability?

- Extra Perks Valued: Do the additional benefits add meaningful value to your life?

Common Myths & FAQs About Extended Warranties

- "They're all scams."

- Reality: While there are unscrupulous providers, many reputable companies offer legitimate and valuable service contracts. The key is thorough research and understanding the terms.

- "My car is too old/has too many miles."

- Reality: While options narrow, some providers specialize in high-mileage vehicles. You might not get bumper-to-bumper, but powertrain coverage could still be available.

- "I'll just put money aside for repairs."

- Reality: This is a valid strategy, but it requires significant discipline and can be overwhelmed by a single major repair. An extended warranty spreads that risk. Consider your risk tolerance and savings habits.

- "It covers everything."

- Reality: Even "bumper-to-bumper" plans have exclusions (wear-and-tear, maintenance, etc.). Always read the fine print!

- "I have to buy it from the dealer."

- Reality: While dealers offer plans, third-party providers often offer comparable or better coverage at a more competitive price. Always shop around.

Your Next Steps: Smart Shopping for Peace of Mind

Choosing the right extended warranty isn't a hasty decision; it's a strategic one. Armed with this knowledge, you're ready to confidently compare options and find a plan that truly protects your investment and provides peace of mind on the road.

- Gather Your Car's Info: Have your VIN, mileage, make, model, and year ready.

- Determine Your Needs: Which coverage tier (bumper-to-bumper, powertrain) makes the most sense for you?

- Request Quotes: Contact at least 3-5 different providers (both dealer and third-party) to compare pricing and coverage specifics.

- Read Sample Contracts: Insist on seeing the full terms and conditions, focusing on exclusions and the claims process.

- Check Reviews and Ratings: Verify the reputation of each provider you're considering.

- Ask Questions: Don't hesitate to clarify anything you don't understand before signing on the dotted line.

By taking a systematic approach, you can transform the daunting task of selecting an extended warranty into a clear path toward protecting your vehicle and your wallet. Drive confidently, knowing you've made an informed choice.